Within the ultra-high-net-worth (UHNW) segment, the importance of wealth planning tools and solutions cannot be overstated. As individuals and families amass substantial wealth, the need for effective and comprehensive strategies to manage and preserve wealth becomes imperative.

Wealth planning serves as a fundamental pillar in the financial journey of UHNW individuals, guiding them through intricate complexities and diverse opportunities. To better understand the considerations for this UHNW segment, we spoke to WMI Faculty member Peter Triggs, a tax, trust and wealth planning veteran of 35 years, a Partner at 1291 Group, and previously Head of Regional Wealth Planning and Insurance, and Head of International Private Banking at DBS Private Bank.

Peter highlights that one of the characteristics of UHNW families is that they often have connections to a large number of overseas jurisdictions through property investments, business interests, or family members living abroad. Thus, it is important that an adviser has sufficient knowledge of the different legal systems and tax regimes found around the world.

Peter says, “As a trusted adviser to our client, even though it is not our role to give tax and legal advice, some knowledge of the tax and legal issues that our clients face is essential in order to raise their awareness of the issues and risks they face, what action they may need to take, and what the solutions may look like.”

The second characteristic Peter points out is that UHNW families often have a connection to a family business. Ensuring that the family business can survive through generational change can be complex and difficult to navigate. Thus, advisers will need to be equipped with the necessary tools and solutions to help UHNW families successfully manoeuvre in this journey.

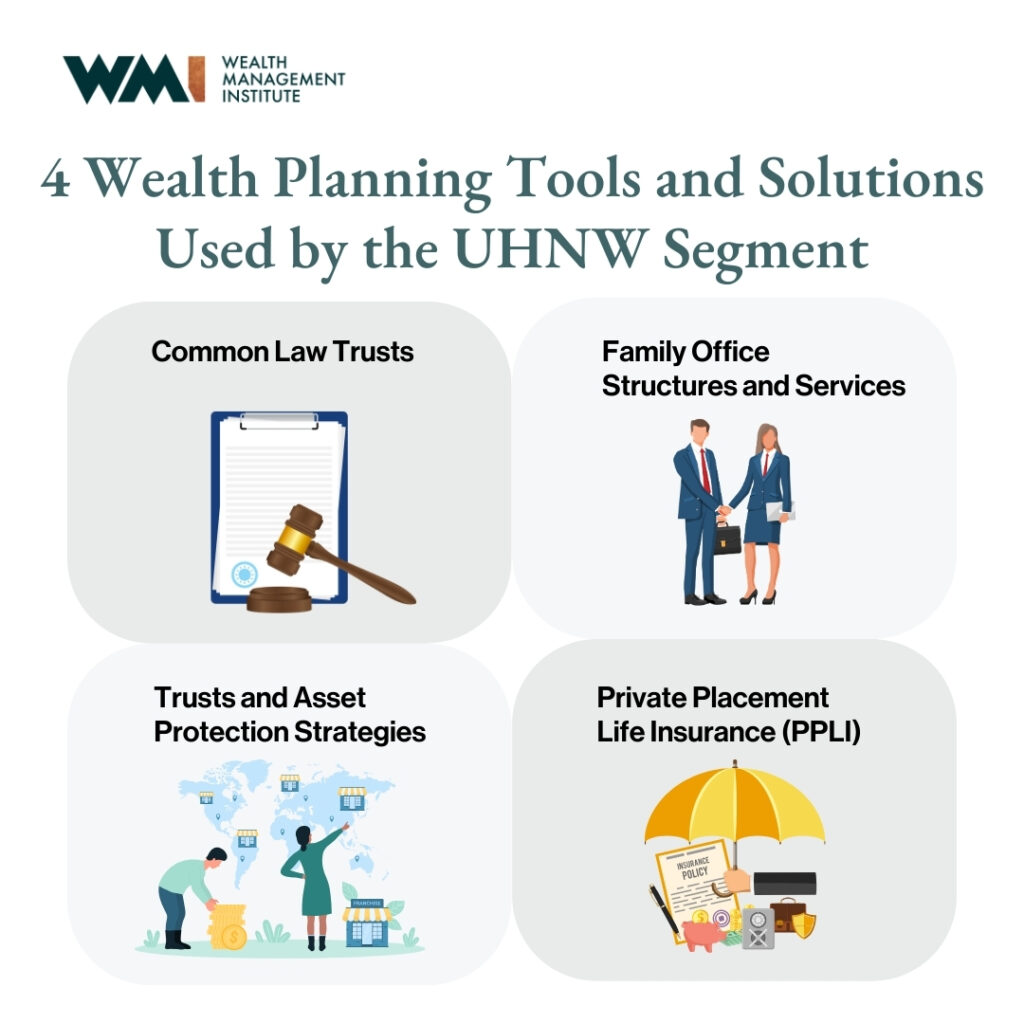

In view of these considerations, there are several key wealth planning tools that the UHNW segment use:

Tool 1: Common Law Trusts

Common Law Trusts are legal agreements where one party (The Trustee) holds and manages assets for the benefit of beneficiaries.

According to Peter, one of the most common tools utilised by the UHNW segment is the Common Law Trust, usually with underlying companies and insurance contracts. These trusts are occasionally structured as Private Trust Companies that can be controlled by family members sitting on the board of the Trust company.

He says, “Where tax exemptions are needed for active trading, these families may set up fund management companies to apply for the Singapore tax exemptions, and often they will include a Family Office where family members and professionals can be employed and manage the fund investments.”

Tool 2: Family Office Structures and Services

Family Offices (FOs) , often involving family members, can be part of a comprehensive wealth planning solution used by the UHNW segment to manage financial and personal affairs.

“Family Offices are a current popular trend in Singapore, and these are specifically covered in Wealth Management Institute (WMI) course programs,” says Peter.

He highlights that some challenges UHNW families face are high foreign taxes in countries such as the US, UK, Japan, and Australia, problems of incapacity in old age, unexpected business litigation impacting personal wealth, divorce, or even generational disagreements amongst children and grandchildren.

By setting up a FO, UHNW families will be able to access professional investment management services, professional tax and legal advice, create diversified portfolios, and engage in due diligence on various assets. Additionally, FO structures can assist with estate planning, tax optimisation, compliance, and can use trusts and charitable foundations to preserve and transfer wealth across generations. Through consolidated reporting and a thorough understanding of their client’s needs and goals, FOs can play a crucial part in ensuring that the UHNW families’ interests are protected and their wealth is effectively managed to meet their long-term objectives.

UHNW individuals often employ a variety of strategies to effectively manage their trust and assets. According to Peter, these clients are highly skilled at generating wealth, but they also recognise the importance of safeguarding it from potential risks such as litigation, foreign taxes, incapacity, family disputes, and divorce. He says: “Understanding these risks allows for the discovery of appropriate solutions to protect their wealth and facilitate succession to future generations. However, many clients never get around to this planning and wealth can be lost, so the WMI prepares advisers to raise awareness and discuss possible solutions with their clients.”

One frequently used strategy, as noted by Peter, involves transferring asset ownership from personal names to entities like companies, insurance companies, trust companies, or a combination thereof. For maximum asset protection a transfer to an irrevocable discretionary trust id usually advised. Additionally, there is a trend among UHNW individuals to shift ownership from onshore jurisdictions to offshore ones, where legal matters are simplified, and certain taxes, like stamp duties, may not be applicable.

Tool 4: Private Placement Life Insurance (PPLI)

UHNW families also often purchase PPLI contracts, a multi-jurisdictional, tailored, wealth planning tool available on an exclusive basis to UHNW families. Peter stated: “Using these insurance contracts as an asset holding vehicle is often found with the very wealthy as it provides investment flexibility, with cost-effective life insurance, privacy, and usually significant tax benefits.”

Conclusion

Peter emphasises the great Wealth Transfer occurring now in the Asia Pacific region and highlights the importance of professionals in this area fully understanding the client’s needs and goals before providing advice. Asking relevant questions and understanding the UHNW segment and their family demographic, type and location of assets, and future plans is critical to being a competent adviser who can help clients address concerns and discover issues they may not have been aware of.

The Wealth Management Institute’s (WMI) Certificate in Succession and Wealth Transfer is one of the distinct modules for our signature programme ‘Certified Family Office Practitioner’, which is designed to provide the skill set for those who are aspiring practitioners for the Family Office, and to provide a comprehensive understanding of the Family office perspectives, internal dynamics and structural setup.

The Certificate in Succession and Wealth Transfer is designed to equip the practitioner with the knowledge and skillsets to guide UHNW families through complex circumstances including wealth succession to the next generation, cross-border compliance, and wealth protection.

“How are practitioners navigating through this landscape and how well-equipped are they to assist? This is where the WMI courses for practitioners come in,” Peter adds.

Participants who successfully complete the programme will be awarded:

Modules

Full Fees (S$)

Before GST

After GST

Company-Sponsored

Modules

Full Fees (S$)

Before GST

After GST

Singaporean Aged Below 40 / PR

Singaporean Aged 40 & Above

Modules

Fees after Subsidy (incl. of GST)

Category

2

1

Not Applicable

1 For Singaporeans aged 40 and above, you are eligible to utilise the SkillsFuture Credit (Mid-Career) further to offset your course fee after the IBF subsidy.

2 Fees shown are after IBF-STS funding assuming students meet the minimum academic standards outlined by IBF and are physically based in Singapore. The fees are also subject to IBF accreditation approval for all modules.

Modules

Full Fees (S$)

Before GST

After GST

Singaporean Aged Below 40 / PR

Company Sponsored/Self Sponsored

Singaporean Aged 40 & Above

Company Sponsored/Self Sponsored

Core Modules

Full Fees (S$)

Before GST

Singaporean Aged Below 40 / PR

Singaporean Aged 40 & Above

Company Sponsored/Self Sponsored

Company Sponsored/Self Sponsored

Note:

In addition to Course Fees, each participant will also be charged a non-refundable and non-claimable application fee of S$85 (including GST).

This programme is pending accreditation by the Institute of Banking and Finance (IBF). When accredited, Singaporeans and Permanent Residents will be eligible for funding support of up to 70% course fee subsidy under the IBF Standards Training Scheme (IBF-STS).

Fees shown are after IBF-STS funding. Subsidised fees apply upon participants’ successful completion of the programme, which includes (i) fulfilling minimum attendance requirements and (ii) passing all relevant assessments.

Subsidies are subject to change by IBF and fees will be adjusted based on prevailing funding rates. Click here to read more about funding support for IBF-STS, and terms & conditions governing registration, payment, cancellation, deferment and no-show.

The information above is correct at the time of publication. Wealth Management Institute reserves the right to amend the fees and/or terms and conditions as appropriate.

Participants who successfully complete the programme will be awarded:

Modules

Full Fees (S$)

Before GST

After GST

Company-Sponsored

Modules

Full Fees (S$)

Before GST

After GST

Singaporean Aged Below 40 / PR

Singaporean Aged 40 & Above

Modules

Fees after Subsidy (incl. of GST)

Category

2

1

Not Applicable

1 For Singaporeans aged 40 and above, you are eligible to utilise the SkillsFuture Credit (Mid-Career) further to offset your course fee after the IBF subsidy.

2 Fees shown are after IBF-STS funding assuming students meet the minimum academic standards outlined by IBF and are physically based in Singapore. The fees are also subject to IBF accreditation approval for all modules.

Modules

Full Fees (S$)

Before GST

After GST

Singaporean Aged Below 40 / PR

Company Sponsored/Self Sponsored

Singaporean Aged 40 & Above

Company Sponsored/Self Sponsored

Core Modules

Full Fees (S$)

Before GST

Singaporean Aged Below 40 / PR

Singaporean Aged 40 & Above

Company Sponsored/Self Sponsored

Company Sponsored/Self Sponsored

Note:

In addition to Course Fees, each participant will also be charged a non-refundable and non-claimable application fee of S$85 (including GST).

This programme is pending accreditation by the Institute of Banking and Finance (IBF). When accredited, Singaporeans and Permanent Residents will be eligible for funding support of up to 70% course fee subsidy under the IBF Standards Training Scheme (IBF-STS).

Fees shown are after IBF-STS funding. Subsidised fees apply upon participants’ successful completion of the programme, which includes (i) fulfilling minimum attendance requirements and (ii) passing all relevant assessments.

Subsidies are subject to change by IBF and fees will be adjusted based on prevailing funding rates. Click here to read more about funding support for IBF-STS, and terms & conditions governing registration, payment, cancellation, deferment and no-show.

The information above is correct at the time of publication. Wealth Management Institute reserves the right to amend the fees and/or terms and conditions as appropriate.

Participants who successfully complete the programme will be awarded:

Modules

Full Fees (S$)

Before GST

After GST

Company-Sponsored

Modules

Full Fees (S$)

Before GST

After GST

Singaporean Aged Below 40 / PR

Singaporean Aged 40 & Above

Modules

Fees after Subsidy (incl. of GST)

Category

2

1

Not Applicable

1 For Singaporeans aged 40 and above, you are eligible to utilise the SkillsFuture Credit (Mid-Career) further to offset your course fee after the IBF subsidy.

2 Fees shown are after IBF-STS funding assuming students meet the minimum academic standards outlined by IBF and are physically based in Singapore. The fees are also subject to IBF accreditation approval for all modules.

Modules

Full Fees (S$)

Before GST

After GST

Singaporean Aged Below 40 / PR

Company Sponsored/Self Sponsored

Singaporean Aged 40 & Above

Company Sponsored/Self Sponsored

Core Modules

Full Fees (S$)

Before GST

Singaporean Aged Below 40 / PR

Singaporean Aged 40 & Above

Company Sponsored/Self Sponsored

Company Sponsored/Self Sponsored

Note:

In addition to Course Fees, each participant will also be charged a non-refundable and non-claimable application fee of S$85 (including GST).

This programme is pending accreditation by the Institute of Banking and Finance (IBF). When accredited, Singaporeans and Permanent Residents will be eligible for funding support of up to 70% course fee subsidy under the IBF Standards Training Scheme (IBF-STS).

Fees shown are after IBF-STS funding. Subsidised fees apply upon participants’ successful completion of the programme, which includes (i) fulfilling minimum attendance requirements and (ii) passing all relevant assessments.

Subsidies are subject to change by IBF and fees will be adjusted based on prevailing funding rates. Click here to read more about funding support for IBF-STS, and terms & conditions governing registration, payment, cancellation, deferment and no-show.

The information above is correct at the time of publication. Wealth Management Institute reserves the right to amend the fees and/or terms and conditions as appropriate.